Notes_trading

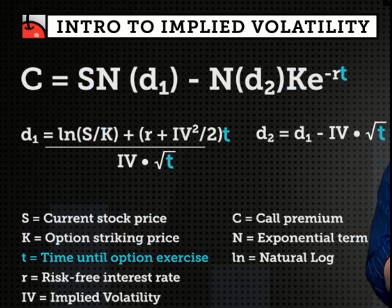

Implied Volatility is an estimation of stock price movement over a period of time, derived from the Black-Scholes Model.

Implied Volatility is an unobservable variable, so we must solve for it using the other Black-Scholes inputs.

- 2.

At its core, Implied Volatility is presented on an annual, one standard deviation basis.

The default timeframe for IV is one year, and since we are forecasting future movement, we can never know the exact move until it happens. Therefore, we must present the value with room for error, which is why it is presented on a one standard deviation basis.

- 3.

Options prices and Implied Volatility have a...

Since the extrinsic value in option prices drive IV, if OTM option prices are high, IV must be high, relatively speaking. If OTM option prices are low, IV must be low, relatively speaking. Therefore, option prices and IV have a positive correlation.

- 4.

In a low IV stock, it is _____________ to buy an ATM/OTM option because the market is forecasting less potential for movement in the stock's price.

If IV is low, that tells us that extrinsic value in the options market is also low, which means option prices across the board are relatively low.

- 5.

In a high IV stock, the option seller _____________ when selling an OTM option because the market is forecasting more potential for movement in the stock's price, which means a higher potential risk for the seller.

When market uncertainty (IV) is high, option prices reflect that. For option sellers, this means more premium for the same strike compared to a low IV environment, or the ability to slide the strike further away from the stock price while still collecting decent premium.

- 6.

If we believe that mean reversion is apparent in implied volatility, that means...

IV tends to be predictable, and that can be seen by looking at any chart of IV or volatility product like VIX, VXX etc. When IV spikes, it tends to collapse over time. When IV has extended periods of low levels, it tends to spike eventually. This is the mean reversion of implied volatility.

- 7.

What is required to determine the annual expected move of a stock's price?

We can determine the expected move of a stock's price by multiplying the IV by the current stock price. IV is presented on an annual, one standard deviation basis, so DTE is not necessary unless we're estimating the expected move of a timeframe less than one year. In that case, we can downgrade the annual expected move by using the expected move formula with a variable DTE input.

- 8.

Expected Move is presented in a +- format because...

Nobody knows where a stock will go for certain, so implied volatility is presented in a +- format.

- 9.

If I sell a strangle (OTM put & OTM call at the same time) in a high IV stock and IV contracts after the fact, I could see a profit because...

Assuming the contraction in IV was not paired with a huge stock price movement, we could see a profit from the IV contraction alone. It's not uncommon to see large % profits just a few days after a short premium trade is deployed if there is a big IV contraction and little to no movement in the stock's price.

- 10.

Implied Volatility "Mean Reversion" refers to:

Historically speaking, IV tends to revert back to its mean, so when we see a spike in IV, we strategize for a contraction towards the mean. When we see very low IV, we strategize for expansion towards the mean.

- 11.

The "buy low, sell high" methodology translates well when talking about implied volatility and mean reversion:

Because stock price movement is pretty random, we strategize around movements in implied volatility instead. We have seen mean reversion in implied volatility through history, so we tend to sell premium when IV is high, and use debit strategies when IV is low.

- 12.

Select strategies that typically benefit from an IV contraction after they're placed:

Most premium-selling strategies would benefit from contraction in IV if they were placed in a high IV environment, as long as that contraction was not paired with a huge stock price move against the strategy. A long put is typically hurt from an IV contraction, as the extrinsic value of the option would go down (against the owner).

- 13.

Select strategies that could benefit from an IV expansion after they're placed:

Debit strategies that have a positive vega would benefit from an increase in IV after the trade was placed. Calendar Spreads and Diagonal Spreads are the most common positive vega strategies that could benefit from an IV expansion. A short put and short iron condor are both premium-selling strategies that would not benefit from an expansion in IV, as that would mean extrinsic value has increased against the trader that has already sold the strategy.

- 14.

Realized Volatility is different than Implied Volatility because...

Realized volatility is nothing more than how much a stock price moved over a given period of time. It's very easy to calculate. Implied volatility is much more complex because we are estimating a potential stock price movement based on an option's price. Realized volatility is historical in nature, and implied volatility is forward-looking in nature.

Comments

Post a Comment